At a recent meeting of the PBBC with the British Embassy in Manila, we were presented with statistics of the latest economy and trade with the UK.

Economy

| Metric | 2019(year end) | 2020(year end) | 2021(Forecast) |

| GDP Growth | 5.9% | -9.5% | 6.5% to &.5% |

| Headline Inflation Rate | 2.5% | 2.6% | 2% to 4% |

| Unemployment Rate | 5.3% | 8.7% | 7% to 9% |

| Overseas Remittances | £22.08 bn | £22.06 bn (-0.9%) | 4% |

| Debt to GDP Ratio | 39.6% | 55.5% | 57% |

| Credit Ratings | Fitch: BBB (positive) | Fitch: BBB (stable) | |

| S&P: BBB+ (stable) | S&P: BBB+ (stable) | ||

| Moody’s: Baa2 | Moody’s: Baa2 (stable) |

Sources: PH National and Economic Development Authority, Philippine Statistics Authority, and PH Bureau of the Treasury

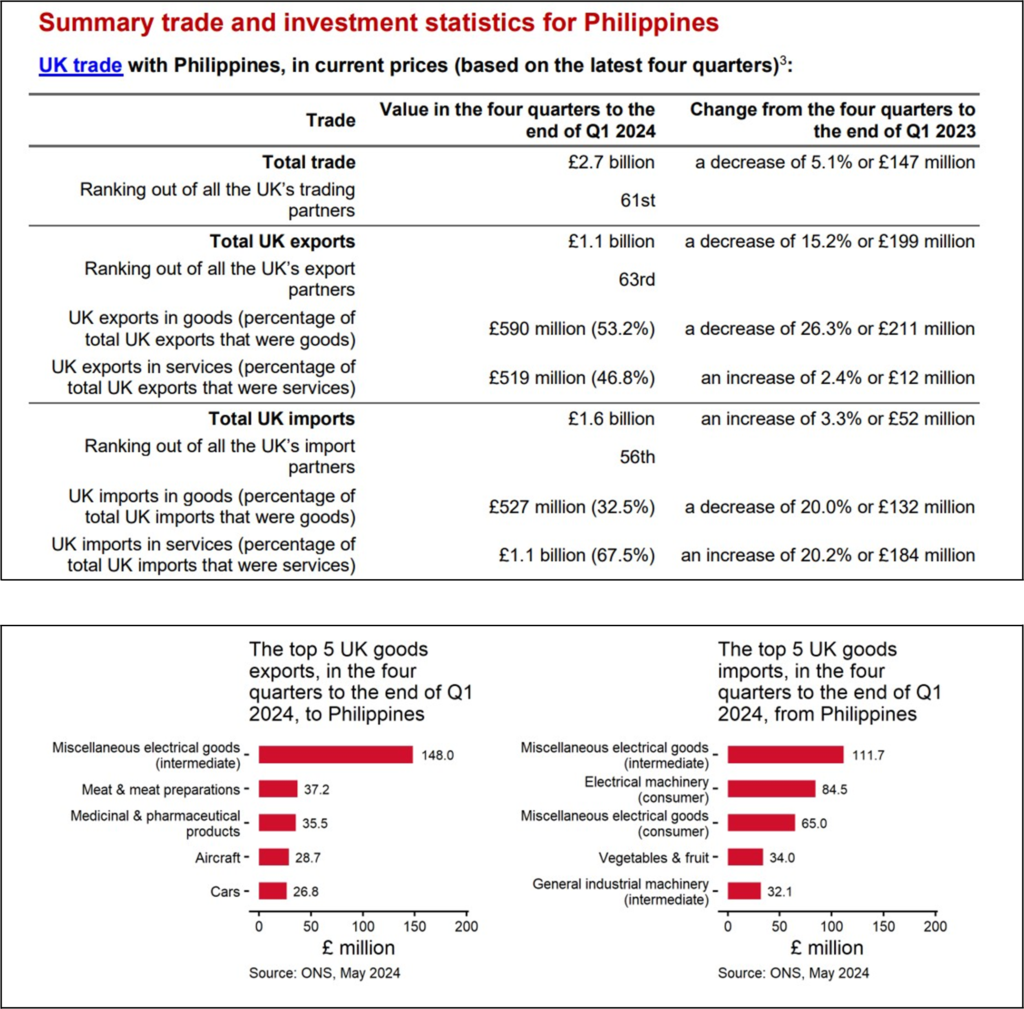

Trade with the UK

Headline Statistics (released February 2021)

Total trade in goods and services (exports plus imports) between the UK and Philippines was £1.7 billion in the four quarters to the end of Q3 2020, a decrease of 21.8% or £468 million from the four quarters to the end of Q3 2019. Of this £1.7 billion:

- Total UK exports to Philippines amounted to £796 million (a decrease of 29.2% or £328 million)

- Total UK imports from Philippines amounted to £886 million (a decrease of 13.6% or £140 million)

The impacts of the lockdown restrictions are starting to show in the statistics. These figures still include around 5 months of normal trade so there will be some lag.

Figures courtesy of: The British Embassy, Manila

Recent Comments